Our Resources

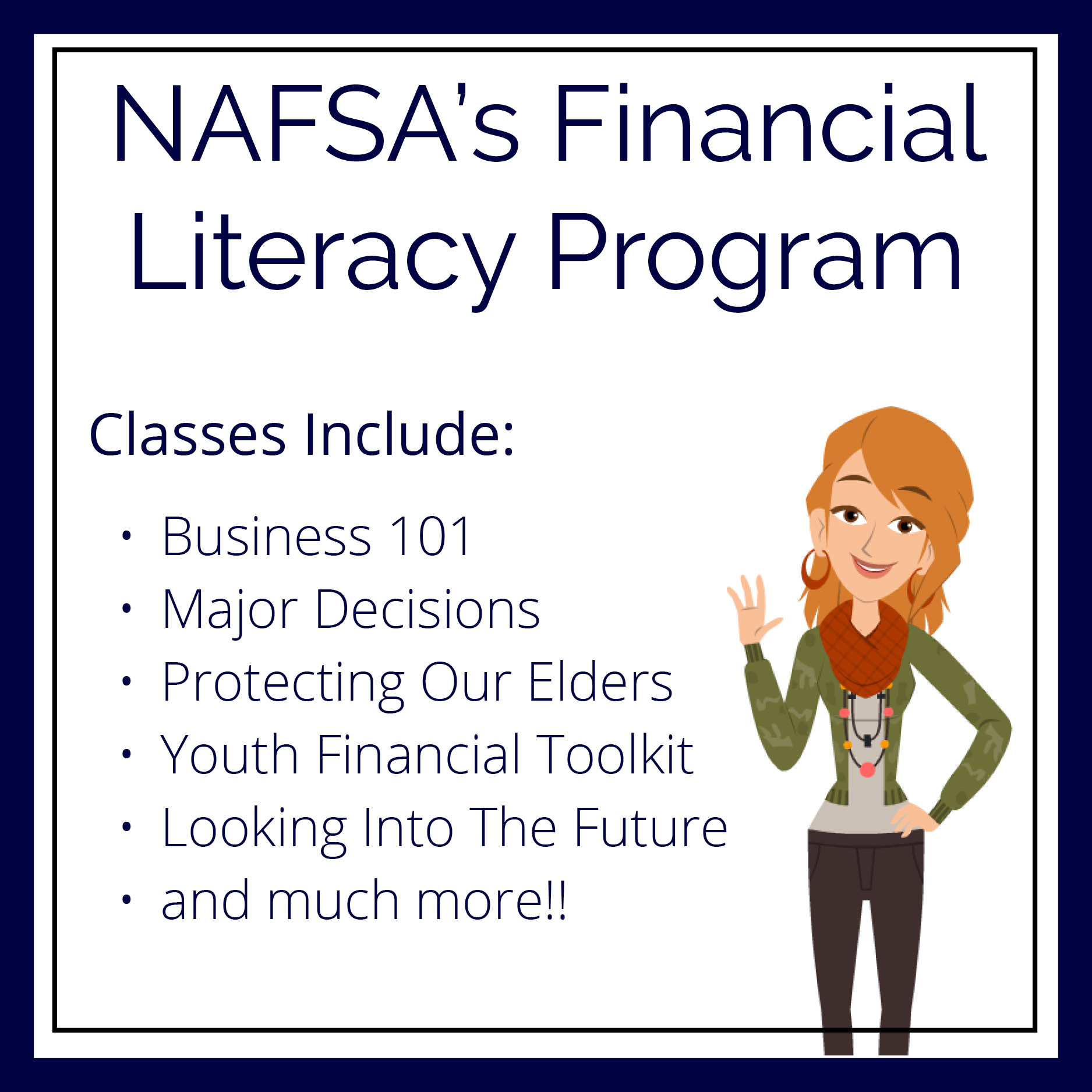

A Digital Financial Literacy Program

Too many consumers mismanage their budgets, make uninformed investment decisions, and fail to properly plan for the future. NAFSA is committed to empowering people with the skills they need to change this trend and thrive financially. NAFSA’s Financial Literacy Program offers an assortment of digital modules covering a wide variety of financial topics, including building emergency savings, mortgage education, and retirement planning.

Tribal Online Lending Best Practices

NAFSA has developed Best Practices for the exclusive use of all NAFSA Members as it relates to their Tribal Online Lending businesses. We believe these Best Practices will help ensure consumer protection, quality service, and positive customer and industry interactions during the life of the loans made by tribal lending entities who are NAFSA members. Our Best Practices apply to all stages of the loan, including marketing, origination, servicing, collecting, and ongoing data privacy.

The Latest Financial News

Yellen Agrees to Stay on as Treasury Secretary Through End of Biden’s First Term

Treasury Secretary Janet Yellen agreed to remain in her position through the rest of Biden’s presidential term as the White House faces growing challenges like the need to raise the country’s borrowing limit. People began speculating about her decision as inflation...

More Consumers Rolling Over Credit Card Debt from Month-to-Month

A new Bankrate report released last week found that the number of adults carrying credit card debt from month to month jumped six points from last year to 35 percent. It also found that roughly 46 percent of credit card holders don’t pay their cards off in full each...

Credit Card Rates Poised to Hit 40-Year High This Year

Credit card interest rates are expected to reach an average of 20.5 percent by the last week of 2023, up from 19.6 percent in the last week of 2022. This is the highest average seen in 40 years, which is painful for consumers facing increased borrowing costs as the...